Forecasts are everywhere, all of the time. The problem with forecasts, as you know, is that they are almost always wrong. While forecasting is used in many different areas of life, including politics and sports, the two most common areas you’ll hear about forecasting are weather and financial markets. Meteorologists, something I actually wanted to become at one point in my life, are well known for being wrong.

Just think about the daily weather forecast you see on your local news station. Are you happy when they call for a high of 70 degrees when the “actual” high is only 55? When it rains when they were calling for “partly sunny skies”? “How can they be so wrong?” is something you probably thought.

Forecasting financial markets is very similar. Current conditions and past data are entered into computers, assumptions are made about the future, humans review the outputs, updating and editing where necessary, and then they publish it as a forecast. The big difference here is that assumptions are utilized to fine-tune the forecast. In order to predict the future, you assume that something will or will not happen, and to what degree.

Herein lies the issue – no one can predict the future. No matter how much past data you use, no matter how certain you are about your assumptions you make about the future, your forecast will be wrong. Why is this? Unforeseen events, and they seem to happen relatively frequently in the life of an investor.

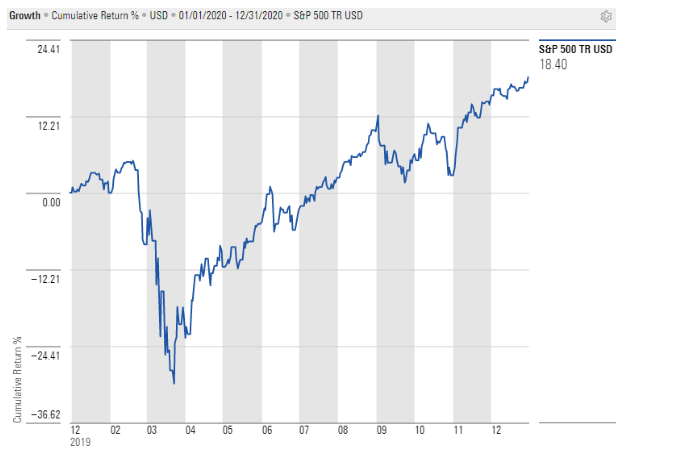

At the end of 2019, the Wall Street Journal published a story that summarized S&P 500 Index forecasts for 2020. China/U.S. trade deals (remember that issue?), falling earnings, and strong consumers were mentioned. The eight firms that the paper studied for the article had the average return for 2020 coming in at 3% (Otani, 2019) . Then, this happened:

No one could have predicted Covid, and the pandemic that it caused. Nor could anyone, even during March of 2020, have predicted that markets would bounce back so forcefully to end 18% higher by the end of the year. Forecasts that didn’t include any macro issue like Covid called for only a 3% return and the S&P 500 Index, even after you factor in Covid shutdowns, returned six times that!

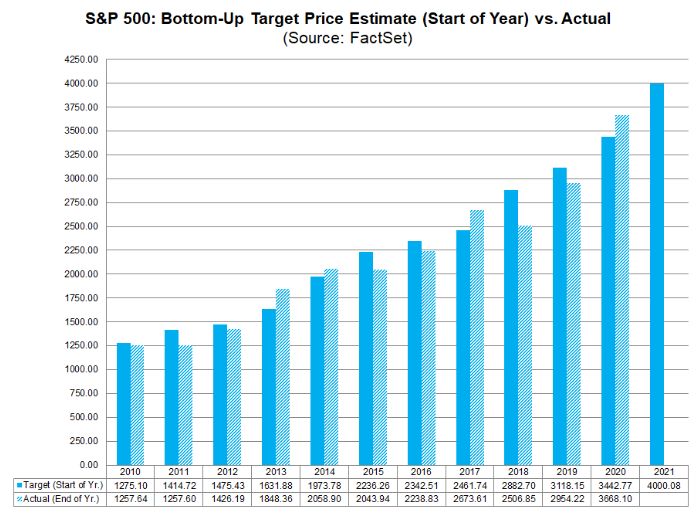

This is just one example of something that caused markets to get derailed, causing forecasts to be revised and altered. Going back over the past twelve years, the average forecaster has been wrong about the performance of the S&P 500 every single year:

The average “miss” is approximately 8.2% over this time frame.

The same is true in the bond market and trying to forecast interest rate movements. According to BlackRock, after reviewing interest rate predictions from 1992 through 2020, most economists got just the direction of the ten-year Treasury yield wrong, let alone the actual ending value.

For 2021, they calculated the average forecast for the 10-year Treasury yield to be 1.15%. It ended the year at 1.52%. Another example is the number of Fed rate hikes expected by the market. Just last fall, the expected number of hikes for 2022 was close to zero. As of March of 2022, seven hikes are now expected. No doubt, these expectations will change as the year progresses, and markets will re-price accordingly.

Investment decisions should not be made on forecasts and expectations; however they should continue to be based on goals and risk tolerance. Asset allocation is key, and is the main driver of returns. We continue to promote this, even in these times of uncertainty and volatility.