You may have heard about the new tax legislation that recently passed and your feelings on it may vary depending on your viewpoint. After all, each beholder has a unique set of eyes. Regardless of how you feel about the political or fiscal ramifications of the new legislation, some of the provisions within it could potentially impact you and your family.

The One Big Beautiful Bill Act (OBBBA) was signed into law on July 4, 2025. (And yes, that is the official name of it.) It brings sweeping and permanent changes to U.S. tax policy. Here’s a breakdown of some the most impactful provisions:

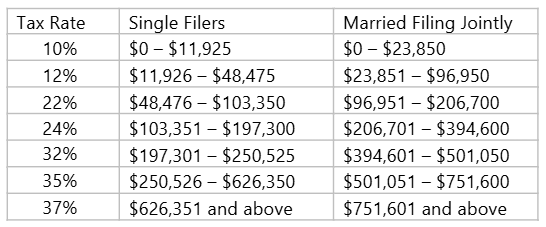

Tax Rates

Tax rates are now permanent, and income brackets will adjust annually for inflation.

2025 Marginal Rates and Income Brackets

Standard Deduction

The standard deduction in 2025 is increased to $15,750 for single filers and $31,500 for joint filers, adjusted annually for inflation thereafter.

SALT

Temporary changes to the state and local tax “SALT” deduction. Increased from $10,000 to $40,000. This applies to households earning $500,000 or less. The deduction limit will increase by 1% annually through 2029, reaching approximately $42,000, before reverting to $10,000 in 2030. This provision is of particular importance for residents of: New York, Washington D.C., Maryland, California, Utah, and Virginia.

Deduction for Taxpayers 65+

A new deduction will be available for taxpayers aged 65+. A new $6,000 tax deduction for individuals age 65 and older (married couples where both spouses are 65+ can claim $12,000), available from 2025 through 2028. This is in addition to the standard deduction and the existing senior-specific deduction (currently $2,000 for singles, $3,600 for couples). There are income eligibility requirements, full deduction available for: single filers earning up to $75,000 or joint filers earning up to $150,000. The deduction phases out at a 6% rate above those thresholds and is fully phased out at $175,000 (single) and $250,000 (joint).

Estate & Gift Tax Exemption

This is permanently increased to $15 million per individual (or $30 million for married couples), beginning in 2026 and indexed for inflation thereafter. Previous tax laws had a “sunset” provision. This new law should offer long-term planning certainty.

For example, the 2025 exemption is $13.99 million per individual; without OBBBA, it would have dropped to ~$7 million in 2026.

Changes for 529 Plans

Beginning in 2026, the new law will allow withdraws up to $20,000 per year, tax-free, for a wide range of grades K–12 and career-related expenses (previously, 529s only covered up to $10,000/year for K–12 tuition). The new expense items include: curriculum materials, tutoring services, standardized test fees, dual enrollment fees for college courses taken in high school, trade school tuition and materials, workforce training and credentialing programs recognized under federal law.

Auto Loan Interest Deduction

A new provision allows for an auto loan interest deduction (for loans originated between Jan 1, 2025 and Dec 31, 2028): Up to $10,000 per year, no itemization required. Applies to personal-use vehicles only (not commercial, fleet, or leased vehicles). Eligible vehicle types include cars, SUVs, pickups, vans, motorcycles, and EVs, as long as they’re assembled in the U.S. (Taxpayer and auto dealership reporting requirements apply).

Charitable Giving

Charitable giving changes starting in 2026. Taxpayers who don’t itemize can deduct up to $1,000 for single filers ($2,000 for married couples filing jointly). This applies to cash and goods donations made to qualified 501(c)(3) organizations. Notable exclusions include political donations, crowdfunding gifts, and donor-advised fund contributions. You must retain written acknowledgment for donations over $250.

Other Notable Provisions

Child Tax Credit Expansion: Increased to $2,200 per child, with a refundable portion of $1,400, both indexed for inflation (eligibility restrictions and income limits apply).

Tip & Overtime Relief: Workers can deduct up to $25,000 in tips and $12,500 in overtime pay (or $25,000 for joint filers), through 2028 (eligibility restrictions and income limits apply).

The Alternative Minimum Tax (AMT) has been adjusted so it doesn’t catch millions of filers in 2026 and beyond.

Business-Specific Provisions

100% Expensing for Capital Investments: Businesses can immediately deduct the full cost of new factories and improvements.

Pass-Through Deduction Made Permanent: The 20% deduction for qualified business income (QBI) is now permanent, with expanded eligibility.

That’s a lot to digest. The entire bill is over 800 pages long and many of the details are still being clarified. One note is that any use of the word “permanent” in regards to tax legislation simply means it is not scheduled to sunset – things could be changed by a future Congress. But now that we know a lot more about the details of the tax legislation and it’s officially law, we’re in a much better position to do tax and estate planning. If you have any questions about any of these provisions and how they may impact you, please contact us!

Sources include: Journal of Accountancy, CNBC, The Wall Street Journal, USA Today, Kitces.com, and Forbes